Last-Minute Planning for the Not-Too-Distant Future

by Lyn Dippel

March 2017/April 2017

While 50th anniversaries are often cause for hearty celebration, not everyone feels as celebratory about their 50th birthday. Many  of us have not had an opportunity to save as much as we would have liked or had the time to do our own financial planning.

of us have not had an opportunity to save as much as we would have liked or had the time to do our own financial planning.

Turning 50 can be a wake-up call that there isn’t much time left to get serious before it is too late.

The good news is our highest earning years are often in our 50s. In addition, special catch-up savings opportunities are available to people over 50. This creates a chance to make a giant leap toward readiness.

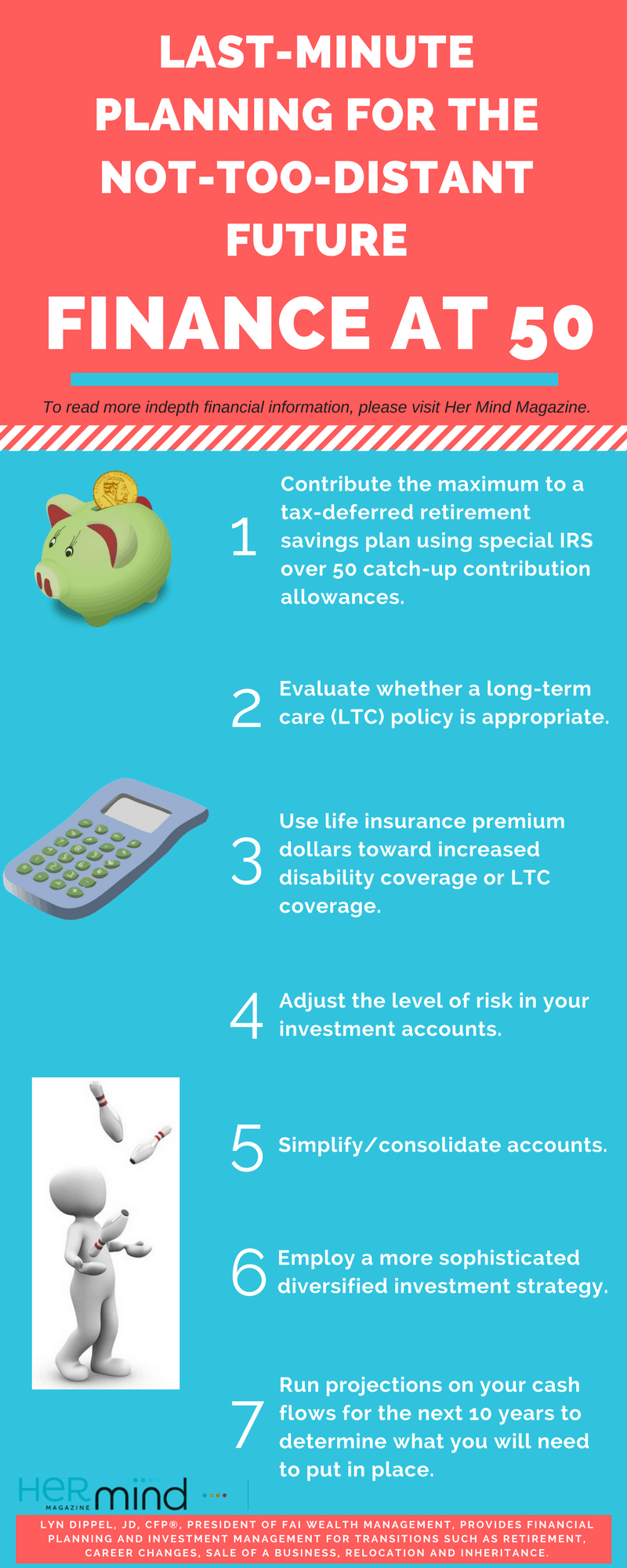

Here are seven actions with impact to consider once you turn 50:

1 Contribute the maximum to a tax-deferred retirement savings plan using special IRS over 50 catch-up contribution allowances:

• If you are employed, take advantage of your employer’s 401(k) or 403(b) plan. The IRS allows contributions of up to $24,000 a year if you’re over 50.*

• If you are self-employed or have a small business with young employees, start a defined benefit plan which will provide an opportunity for you to save up to $255,000 annually pre-tax.*

• If you are self-employed with no employees, you can set up an individual 401(k) and make contributions as both the employee and employer up to a total of $59,000 a year.*

*Specific IRS guidelines apply so see your tax or financial advisor for more details on these plans.

2 Evaluate whether a long-term care (LTC) policy is appropriate:

This is a personal choice based on family history, the ability to self-insure, the ability to pay for premiums and current health. The earlier you purchase a policy, the lower your annual premium will be for the remainder of your life. Keep in mind that your ability to qualify may be affected if you develop a health condition before you have secured a policy. If you are disabled in an accident or non-age related event, you may need care. Neither disability nor medical insurance will cover these expenses. One thing to keep in mind: The earlier you purchase a policy, the longer you will potentially be paying premiums. Your insurance or financial advisor can help you optimize your choices.

3 Use life insurance premium dollars toward increased disability coverage or LTC coverage:

You may be able to save some insurance costs by evaluating whether you still need life insurance at this stage. If education costs are covered or you no longer have dependent children, this may be a good time to reduce or eliminate old policies and put those dollars toward other coverage. Alternatively, some insurance companies now offer the option to convert a permanent life insurance policy into a hybrid policy that includes long-term care coverage.

4 Adjust the level of risk in your investment accounts:

Assuming you have had mostly stock or stock funds in your investment accounts, now is a good time to reduce the risk and add other asset classes to protect against major losses you won’t have time to recover.

5 Simplify/consolidate accounts:

By the time they turn 50, many people have multiple investment accounts and old employer plans. This makes it difficult to understand the overall risk level and to manage all the accounts. In addition, keeping funds in old employer plans can limit your investment choices and can sometimes generate unnecessary fees.

6 Employ a more sophisticated diversified investment strategy:

An overall investment plan includes having a coordinated allocation across all your investment accounts, proactive tax management and most likely the introduction of additional asset classes beyond stocks and bonds (such as real estate funds, commodities or other assets not correlated with the market).

7 Run projections on your cash flows for the next 10 years to determine what you will need to put in place:

Don’t be fooled by simple retirement calculators that rarely take into account your tax situation and other personal details that will have a big impact on your future needs. A financial planner or robust planning software can help you make the most efficient use of your resources and help you evaluate the impact of complex decisions. Analyzing several scenarios under consideration will help you make decisions that reflect both your personal values and your financial goals.

Lyn Dippel, JD, CFP®, president of FAI Wealth Management, provides financial planning and investment management for transitions such as retirement, career changes, sale of a business, relocation and inheritance.